Dealing with an Orlando homeowners insurance claim after catastrophic tornado damage requires a firm grasp of the claim timeline and your legal rights under Florida law. At Kennon Law, our skilled insurance claim lawyers help you document loss and negotiate settlement terms to ensure you receive a fair settlement for every structural loss.

In Summary

A tornado insurance claim in Florida involves a structured settlement period that requires detailed documentation and a clear understanding of your homeowners insurance policy. Navigating the claims process effectively ensures you receive a fair settlement for the full extent of your structural loss.

- Claim Timeline Expectations: The average time to settle claim requests typically ranges from 30 to 90 days, though catastrophic disasters can lead to a prolonged payout duration.

- Immediate Action Steps: You must file a claim promptly to obtain a claim status number and document loss through high-resolution photos, video, and independent contractor estimates.

- Mitigation Requirements: Property owners have a statutory duty to mitigate loss by performing emergency repairs to prevent further damage from rain or theft.

- Florida Legal Protections: Under Florida law, insurance providers are generally required to acknowledge a claim filing within 7 days and provide a financial coverage decision within 60 days.

- Settlement Negotiation: Avoid rushing to accept an initial lowball offer; instead, negotiate settlement terms by comparing the insurer’s estimated costs with actual repair estimates.

- Identifying Bad Faith: If an insurance carrier delays processing or fails to inspect property thoroughly, it may constitute bad faith, necessitating a free consultation with skilled insurance claim lawyers.

- Disbursement Process: Once a claim is approved, the disbursement process for the final settlement should be expedited to allow you to repair structures and replace personal property.

Tornado Home Insurance Claim Timelines

Tornado home insurance claim timelines generally range from a few weeks to several months depending on the severity of the structural loss. While a simple claim might conclude in 30 to 45 days, a catastrophic disaster often forces a prolonged settlement period due to the sheer volume of claims.

The duration of your homeowners insurance claim is influenced by several external and internal factors. When a natural disaster strikes Orlando, insurance providers often face a backlog, which can delay claims significantly. If your damaged property requires an extensive appraisal process or involves complex claims with multiple contractor estimates, the payout duration naturally extends. Below are common variables that impact the average time to settle claim requests:

- Extent of Damage: Total losses take longer to inspect property and calculate depreciation than partial ones.

- Carrier Responsiveness: How quickly the insurance carrier acknowledges receipt of your claim filing.

- Dispute Resolution: Time spent negotiating settlement amounts or addressing lowball offers.

- Catastrophe Response: The speed of the national association or local disaster assistance teams.

Before You File a Claim (Filing a Claim Checklist)

Preparing a thorough checklist before you file a claim is essential for ensuring an expedited and fair settlement. You must collect detailed documentation, including a proof of loss form, repair estimates, and a comprehensive inventory of all personal property impacted by the wind damage.

Before contacting your insurance agent, organize your evidence to document loss effectively. Use your phone to capture high-resolution video and photos of all structural damage and residential debris. Obtain at least two independent contractor estimates to compare against the initial estimated values provided by the insurer. Having this documentation ready helps you mitigate loss and provides skilled insurance claim lawyers with the necessary data to advocate on your behalf.

Prevent Further Damage After a Tornado

Preventing further damage after a tornado is a statutory requirement under most homeowners insurance policies to avoid a claim denial. You should perform emergency repairs, such as tarping roofs or boarding windows, to mitigate loss and protect the property from rain or theft.

When you repair structures temporarily, you must keep every receipt for materials and labor. These costs are typically reimbursable under your insurance coverage as part of the disbursement process. Failing to secure the damaged property could lead the insurance company to deny portions of your compensation if they determine the extent of the damage increased due to neglect. Always inspect property for safety hazards before attempting any mitigation efforts.

The Tornado Claim Process: Step-by-Step Claims Process

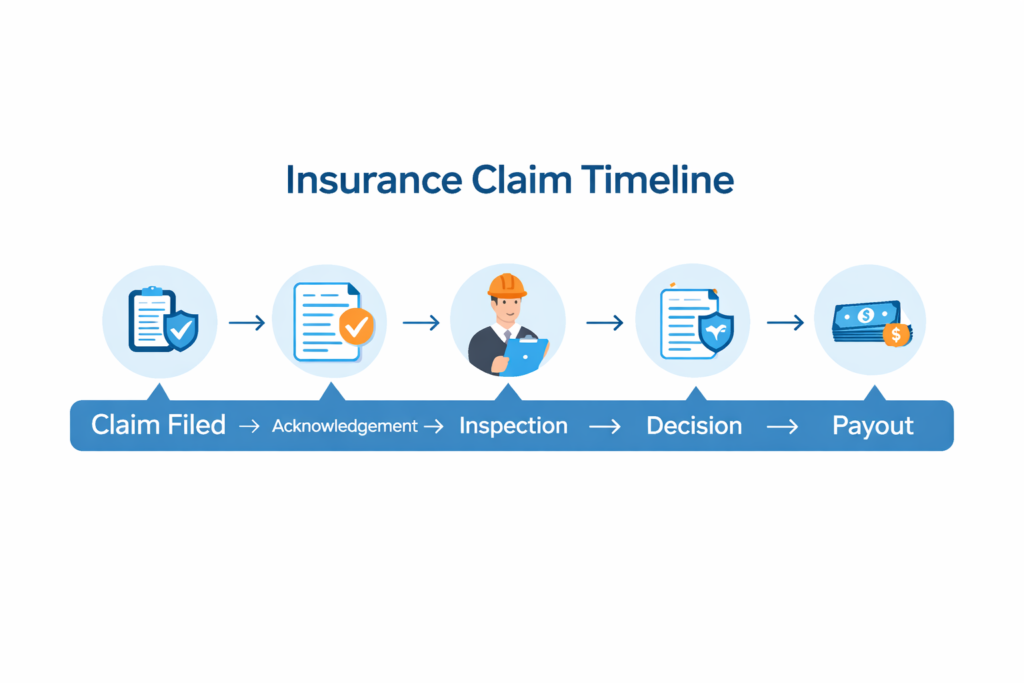

The tornado claim process begins with immediate notification to your insurance company to obtain a unique claim status number. This structured claims process involves a formal claim filing, a thorough investigation by a claims adjuster, and the eventual receiving payment for approved repairs.

Following your initial report, you must document loss and submit proper documentation through the insurance carrier’s portal. Schedule the adjuster inspection as soon as possible, as many homeowners in Florida will be competing for the same property adjuster’s time. During the inspect property phase, accompany the adjuster to point out all structural issues. Keep a detailed log of every phone call, email, and acknowledgement receipt to protect yourself against bad faith tactics or delays.

Timeline by Stage: Average Time for Each Damage Claim Step

The average time for each damage claim step varies, but most Florida home owners can expect a standard progression from filing to final settlement. Generally, the insurance company acknowledges your claim within 7 to 14 days, followed by an investigation phase that can last several weeks.

| Claim Stage | Estimated Duration | Key Action |

| Claim Filing & Acknowledgment | 3 – 7 Days | Insurer issues claim number. |

| Adjuster Inspection | 7 – 14 Days | Adjuster conducts site visit. |

| Investigation & Decision | 30 – 60 Days | Insurance carrier verifies coverage. |

| Disbursement Process | 10 – 20 Days | Receive payout for approved amounts. |

Common Delays After Multiple Damage Claims

Common delays after a natural disaster often stem from a catastrophic surge in home insurance claims that overwhelms local insurance providers. A backlog in the appraisal process or pending repair estimates can cause a prolonged wait for many homeowners.

To expedite processing, you should proactively resolve any documentation gaps and maintain frequent communication with your claims adjuster. If the insurance company makes unreasonable requests or delays, it may be necessary to involve skilled insurance claim lawyers. Frequent follow-ups ensure your claim status remains active and doesn’t get buried under more complex claims in the insurer’s system. Florida law requires companies to act with reasonable speed, so stay diligent.

Understanding Your Home Insurance for Tornado Damage

Understanding your homeowners insurance policy is vital for determining the extent of your financial recovery after a tornado. You must verify coverage limits, identify your deductible amounts, and determine if your insurance policy provides replacement cost or actual cash value.

Most residential policies cover wind damage, but you must check for specific hurricane or storm damage exclusions. Additionally, confirm if you have “Additional Living Expenses” (ALE) coverage, which helps save money on temporary housing while you repair structures. Reviewing the named-peril language in your insurance coverage helps you understand what the insurance company is statutory obligated to pay.

Negotiating a Fair Settlement for Your Damage Claim

Negotiating a fair settlement for your damage claim requires comparing the insurer’s initial offer against independent contractor estimates. If the insurance company provides lowball offers, you should prepare a written counteroffer backed by detailed documentation of the structural loss.

For more complex claims, hiring a public adjuster or consulting with skilled insurance claim lawyers at Kennon Law can provide significant leverage. We help you negotiate settlement terms by calculating the full extent of the total damage. If the appraisal process becomes disputed, having professional representation ensures the insurance carrier treats your residential or commercial claim with the gravity it deserves.

If the Insurer Delays or Acts in Bad Faith

If the insurer delays without cause or fails to process payment for an approved claim, they may be acting in bad faith. Signs of such conduct include denying coverage without a structural investigation or failing to acknowledge receipt of your documentation within statutory timeframes.

If you suspect bad faith, you should send a formal written demand letter to the insurance company. You can also file a complaint with the Florida insurance commissioners. Before filing suit, it is highly estimated that consulting with an attorney will improve your chances of a fair settlement. Kennon Law can help you negotiate on your behalf to ensure the insurance carrier adheres to Florida law.

Special Considerations for Florida Home Tornado Claims

Special considerations for Florida home owners involve strict statutory timelines established to protect policyholders from prolonged delays. Under Florida law, insurance providers must generally acknowledge a claim within 7 days and provide a written coverage decision within 60 days.

The Florida homeowners Bill of Rights provides an expedited framework for catastrophic events. However, you must be aware of specific hurricane deductibles that might apply if the tornado was spawned by a larger tropical system. Many cases in Orlando involve disputed wind damage vs. flood damage, making it crucial to document loss with detailed documentation to ensure your insurance claim is processed correctly and settled fairly.

When to Get Help: Free Consultation and Legal Options

Seeking a free consultation with skilled insurance claim lawyers is recommended when the settlement period becomes prolonged or your claim is unfairly denied. Professional legal help is especially beneficial for complex claims involving total structural loss or disputed repair estimates.

At Kennon Law, we represent homeowners to ensure they receive the full extent of their compensation. If you are facing lowball offers or bad faith delays, we can help you negotiate or proceed to litigation. Contacting us early in the claims process can help save money and time by ensuring your initial claim filing is legally sound and backed by proper documentation.

Quick Checklist: What To Do After a Tornado Damage Claim

- file a claim promptly and obtain a claim number

- document damage thoroughly with photos and receipts

- prevent further damage and keep temporary repair records

- pursue professional help when settlements seem unfair

FAQ

Tornado insurance claim timelines vary, but most are settled within 30 to 90 days. Catastrophic events or more complex claims involving total structural loss can take weeks or months longer. Proactive claim filing and detailed documentation are key to achieving an expedited settlement period.

If an insurance carrier makes lowball offers, you should negotiate settlement by providing independent contractor estimates. Skilled insurance claim lawyers can help document loss and verify coverage to ensure the insurer pays the fair settlement required to repair structures to their initial state.

A standard homeowners insurance policy typically covers wind damage from tornadoes as a structural loss. You should verify coverage limits for personal property and residential repairs. Always check for specific storm damage exclusions or high hurricane deductibles that may apply under Florida law.

Accepting the initial payment may be risky if it doesn’t cover the full extent of structural damage. Often, the initial disbursement process is just a partial payout. Consult an adjuster or attorney to determine if the money offered represents a fair settlement before signing a final settlement release.

The statutory deadline to submit a proof of loss is typically 60 days after the insurance company requests it. Failing to file this proper documentation can lead the insurer to deny your home insurance claims. Always check your specific insurance policy for the exact claim filing requirements.